It seems like pellets and chip markets might be useful for places like California which have 1) extra small trees to think for fuel treatments (conceivably without “industrial logging”, however that is defined, and 2) access to ports. BC seems to be taking advantage of these opportunities.

Again logically there are two options if the use is bioenergy (conceivably this material also could be used for higher-value products). The first is to burn this material for bioenergy in California (not developed well due to pollution standards) or sell to others (which as Matthew points out, involves use of (more) fossil fuels currently for transport.) This might raise all kinds of questions about Asia, for example, and their bioburners’ pollution and climate change calculations.

Anonymous hypothesized here that maybe the answer is availability of supply. If this sounds like a blast from the past, some of us remember the mountain pine beetle infestation in the 80’s in Central Oregon and trying to do something with the dead trees (forty years ago). One idea was to get a waferboard plant in Chiloquin, Oregon. This idea foundered on the shoals of .. supply dependability. It seems like a bit of a theme. I think it’s important not to just conflate this with “litigation about projects”, although that may be a piece of the puzzle. Again logically, a deal could be reached to say (if material x is removed, in y kinds of places, with practices such that z does not happen, to a total amount of a per acreage b, then we will not litigate). Even so, if I were considering investing, I would be very dubious, given our track record. It is interesting to think how Canada can provide adequate assurances for investment but we cannot.

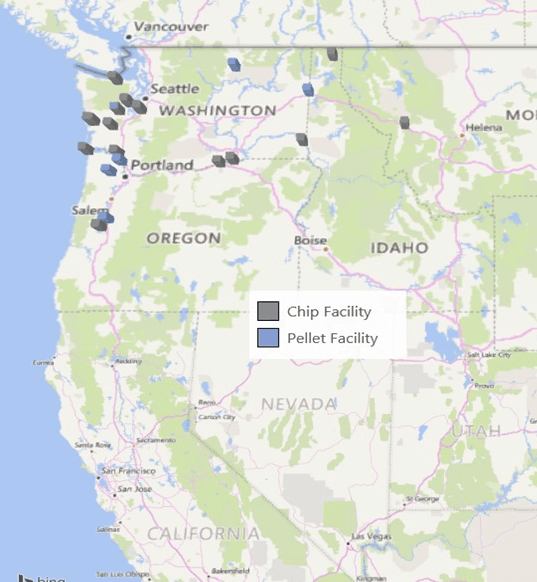

I haven’t yet found an expert on this topic, and am still searching, but a forest economist friend pointed me to this piece that compares the Pacific Northwest to the US south and other sources. First, the authors note that a preponderance of forest land is public compared to the Southern U.S..

One notable difference between the US South and the Northwest is the seasonal (but frequent) occurrence of severe, large-scale wildfires. This is related to a combination of climatic conditions in the PNW, ownership/management intensity and harvest restrictions, all of which have allowed for the build-up of excessive fuel loads in many forest stands. One method proven to be effective in reducing wildfire loss is through the use of fuel-reduction thinning operations, especially on public lands.

Due to this lack of forest management, one analysis estimated that up to 12 million green tons of biomass could be harvested via fuel-reduction thinning over the course of a decade. If this management practice is promoted and implemented, the increase in small log and residual material availability could spur a growth in both wood chip and pellet production.

Ownership/Supply Chain Characteristics

With forestland ownership being primarily public (federal, state and municipal), the fiber supply chain in the US Northwest is somewhat different than in other regions. Public land management is governed by different sets of rules and procedures, and harvesting is conducted at a reduced level compared to private land.

A large portion of private forestland is owned by timber investment management organizations (TIMOs), real estate investment trusts (REITs), and other large landownerships that supply a majority of the timber in the region. Because of the TIMO/REIT influence in the region, tract sizes are generally much larger and small tracts (under 20 acres) are less prevalent than in other regions. There are small-scale landowners as well, but they comprise a much smaller piece of the available volume.

As a result of this fragmented ownership situation, there is not a robust timber dealer/broker network. Large landowners generally negotiate delivered contracts directly with the mills, and they then pay loggers for harvesting services and transportation from the woods to the mill. While there are some stumpage sale contracts in the region, it is not a common practice as it is in the US South.

So there are structural problems compared to the US South (not a robust dealer/broker network) which makes it more difficult to get this material from private land, but this article doesn’t mention the “relatively assured supply” problem from public lands. Seems like if it were a good idea to sell material removed from fuel treatments that California economic development would be on it. Maybe they are.

One of the other structural problems for federal land reliability of supply is contractual. In the Bush Administration we worked to develop stewardship contracts. Congress provided the authority but federal contracts are limited in length- the longest allowed at that time was 10 years. Financial institutions want 20 years to lend the money to contractors for the equipment and related business requirements to do the thinning/stewardship work. The bulk of the material and cost to transport relative to material value were other impediments to federal biomass utilization that we discovered during a focused multi-year examination and development effort as part of the Healthy Forest Initiative. I suspect the Canadian government’s different legal and ownership of the Crown lands and companies creates possibilities that we don’t have in US.

In my experience, transportation costs have always a sticking point at some point, either at the beginning (stifling the start up) or years into the venture (once those costs are discovered to tip the balance sheet to the negative). It has been 30 years since I saw my first biomass operation in the field – I am amazed the same sticking point still exists today.

I guess what was interesting to me is that folks in BC can pay those costs and make money and we can’t.

I’m sure sawmill residues are easier to move than material from scattered units in the woods. And perhaps once the pellet mills are developed based on those residues, then the additional cost of getting the scattered material to the mill can still be supported. I’ve got a couple of traplines out to forest economists that perhaps can still pay off.

Here’s an article on a related topic, from the Feb. 2019 edition of The Forestry Source:

Forest Products Marketplace

California OSB Manufacturing: Holy Grail of the OSB Industry?

By Roy Anderson

In this article, I will explore the feasibility of manufacturing oriented-strand board (OSB) in Northern California, a timely topic in the wake of the Carr, Camp, and Mendocino Complex wildfires that struck the region in 2018. The three fires combined affected nearly 850,000 acres, destroyed nearly 21,000 structures, and tragically claimed nearly 100 lives.

The raw materials used to make OSB can include small-diameter trees. OSB plants typically use large quantities of such materials. Thus, developing a plant in Northern California would provide a cost-effective means of carrying out wildfire-hazard reduction and forest health–management treatments on many thousands of acres each year.

In 2017, North American OSB demand was about 23.1 billion square feet (all references in this article to OSB panel square footage have been normalized to a 3/8-inch thickness basis). The Beck Group’s analysis of OSB end-use markets found that the 2017 demand for OSB within 500 miles of Northern California was about 2.8 billion square feet, or about 12 percent of all North American demand. However, as shown in Figure 1, there are more than 50 OSB plants in North America, but none are less than 1,200 miles from California’s large OSB market. In the next few paragraphs, I’ll briefly explore why this situation exists and then outline the business case for developing an OSB manufacturing facility near the California market.

Why are there no OSB plants in the western US? Quite frankly, I’m not sure. The most likely reason is that in much of the western US a relatively high percentage of the timberland is under the control of federal and state government agencies. Greatly reduced timber harvests on public lands over the last 30 years and a trend of increasing average OSB plant size have combined to reduce the certainty of a cost-effective raw material supply. Indeed, during the early days of the OSB industry, when harvest levels on public lands were higher and the average plant size was much smaller, there were OSB plants operating at various locations throughout the US West.

The Business Case for California OSB

In 2016 and in later work completed early in 2018, the Beck Group, KTC Industrial Engineering, and an OSB industry member worked together to assess the feasibility of developing an OSB plant in Northern California. The key factors evaluated included:

• Raw material supply and cost

• Market-related issues, including product mix, the finished-panel transportation-cost advantage, and product sales values

• Capital and operating costs

• Siting considerations

• Permitting and regulatory issues—always an issue, but especially important in California

A critical decision early in the process was establishing the size of a prospective plant. As our analysis evolved, we moved from a relatively small plant with annual production of about 475 million square feet (MMSF) to a larger plant with a capacity of about 750 MMSF/year. The larger plant would consume about 550,000 bone-dry tons of raw material annually. Our raw-material supply analysis found that topwood from ongoing sawtimber harvests, small-diameter trees from forest-health treatments, and sawmill byproducts, such as lumber trim ends, slabs, and edgings, could supply nearly two times the prospective plant’s annual raw material requirement. As I mentioned in the introduction, the recent wildfires in California, while unfortunate and tragic, may have created a situation in which community and political leaders are ready to fully support a large wood-products manufacturing facility that can utilize the fuel that has built up in the region’s forests.

Regarding markets, we modeled a plant that would produce a mix of commodity OSB sheathing and underlayment products. However, there would be considerable upside if the plant were designed to also produce some value-added, specialty products, such as custom-size panels for export to Asia and panels with flame-resistance or thermal heat shield barrier overlays. At a production volume of 750 MMSF per year, we estimate the nearby annual OSB market size is nearly four times larger than the capacity of the plant. We also estimate that a Northern California OSB plant would enjoy an average of about a $35/MSF freight cost advantage over other North American OSB producers when shipping product to market. That amount is about 15 percent of the long-term average OSB sales value.

Our research also found that regulatory and permitting issues are notoriously difficult processes in California. One strategy identified for mitigating these issues was to utilize natural gas for the process steam used in manufacturing OSB. While this approach creates higher operating costs than the more-traditional practice of combusting byproducts (bark, fines, and so on), is the higher costs are offset by the ability to operate a competitively scaled plant in California with emissions that are well within allowable levels. We also believe there are opportunities for strategic partnerships that may allow for more flexibility in navigating the permitting process and allow for utilization of byproducts.

We also developed a comprehensive financial model for the prospective plant. Our analysis indicates that, while building a plant is a significant capital investment, the project would have solid financial returns. There is also potential for upside to financial performance through strategic partnerships to reduce operating costs, leveraging incentive programs (tax breaks, low-interest loans, etc.), and diversifying the product mix to include some higher-value items.

I would love to hear your thoughts about this article. If you are interested in pursuing this concept as a developer of an OSB plant, please contact me to learn more.

Roy Anderson is vice-president of the Beck Group (beckgroupconsulting.com), a forest-products consulting service based in Portland, Oregon. Contact him at 503-684-3406 or [email protected].