Pretty sure this isn’t about wildfire risk based on this map.

Pretty sure this isn’t about wildfire risk based on this map.

The Hotshot Wakeup is best at covering this stuff, but we have folks in the media saying that wildfires will get worse, due to climate change.

Meanwhile, we also have the military-industrial complex developing early sensing and unpersonned firefighting helicopters, which conceivably can reduce spread.

We have fire retardant litigation, the EPA working on permits, one fire retardant contract that is under protest and can’t be awarded, and one for more “environmentally friendly” retardant that eats away at the metal in aircraft such that some will not be available for the 2024 fire season.

I’m not sure how scientists can model the climate fingerprint of all that.

We have power companies shutting off power (so conceivably we will have fewer ignitions) although their approaches raise questions (in Colorado the PUC will be investigating), and maybe also have unequal impacts based on socioeconomic conditions.

More than 150,000 Xcel customers lost power because of the intentional shut offs or damaged equipment during the winds that included gusts of nearly 100 mph Saturday into Sunday. As of 10 a.m. Wednesday, the company reported 75 outages affecting 929 customers.

Residents and at least one food bank were forced to toss unrefrigerated food, and several metro Denver schools were closed through Tuesday. Employees at a Boulder wastewater treatment plant had to scramble to make sure raw sewage didn’t flow into Boulder Creek when power was cut to the plant’s two electric substations.

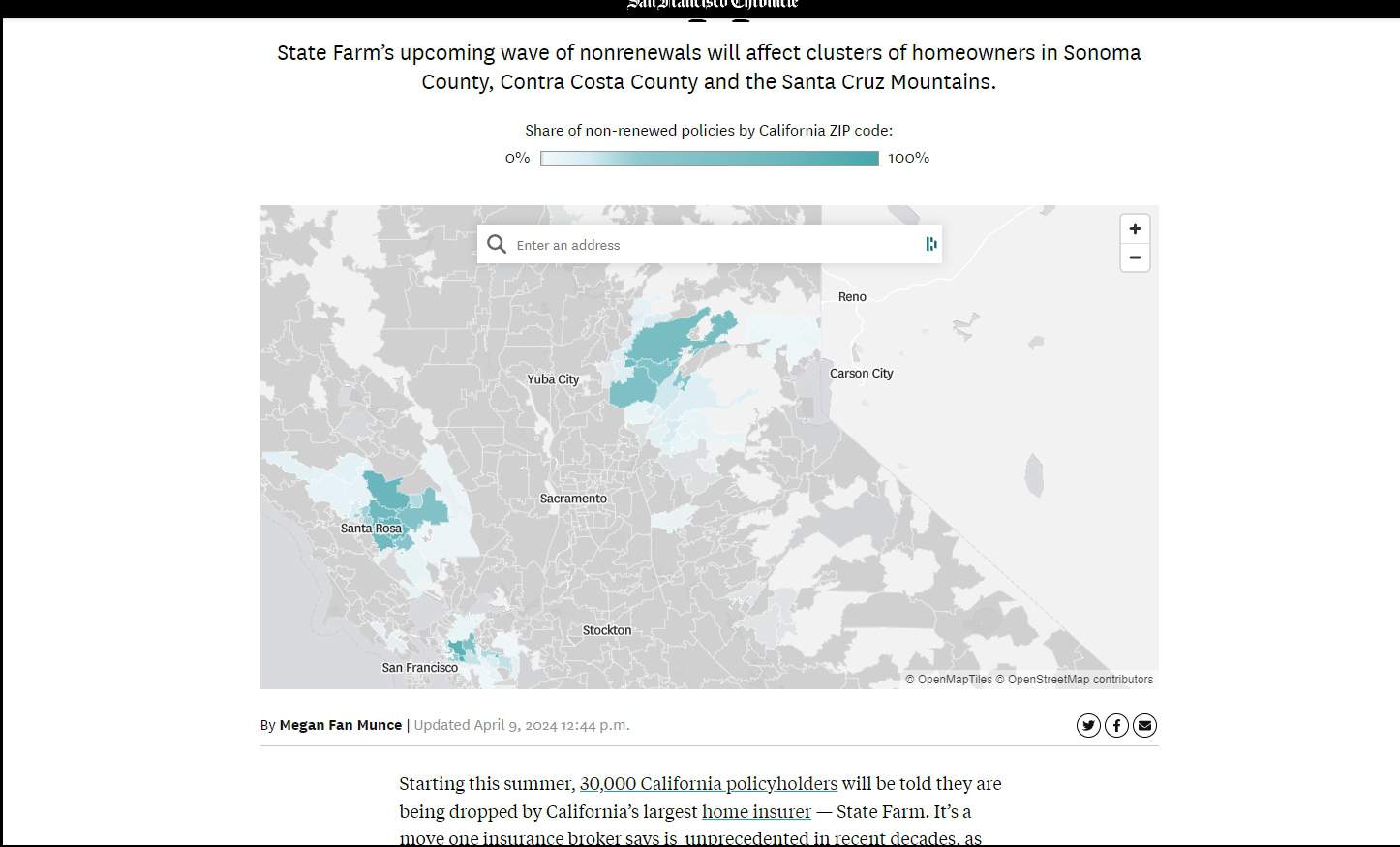

Then there’s this fascinating story from the San Fran Chronicle on for which zip codes State Farm will be non-renewing policies. We can check out the map and see .. whatever it’s about, it’s not about wildfire.

According to the article:

State Farm wrote in state filings that it would not renew policies “that present the most substantial wildfire or fire following earthquake hazards, or that are in areas of significant concentration.”

And probably not about earthquakes. If you go to that link it says:

Last October, Marc Snyder’s insurance company informed him it wouldn’t be renewing his homeowners insurance this year for a reason he had never heard before: density.

The letter from Liberty Mutual said Snyder’s home was “located in a region where the dwellings are considered to be too densely concentrated for us to continue to provide coverage.”

But increasing density is supposed to be good for climate change, and climate change is supposed to be bad for wildfires. That’s what I mean by the circle of life.. California’s policies are to increase density. Anyway, sounds like there will be much work for PUCs and insurance commissions to investigate in terms of maps, and I hope they dig deeply. Perhaps California, as well funded as it is, can figure the insurance/power company conundrum out and let the rest of us know what they find.

High density housing in the WUI is a concern because houses are fuel and one cannot chop their neighbor’s house down to remove the fuel. Why is 100 feet used to define the defensible space zone for a structure? Studies at the Missoula Fire Science Lab found that at a distance of 100 feet or more, structures would not ignite from radiant heat generated by wildfire. When houses are closer than 100 feet, and there are no fire managers available to ensure the structure fire is contained, there is a decent chance the fire will spread from structure to structure due to radiant heat. The closer the houses, the high the probability of spread. For high density housing in the WUI, defensible space cannot be maintained unless all of the homeowners within 100 feet of each other have done the work and have clean gutters/roof, removed surface fuels, removed debris from around the foundation, have screened-vents with less 1/8 inch or less mesh, limbed up their trees, etc.

Somewhat unrelated and not a TSW topic, I don’t think the “cause” of the housing crisis is too few homes. The cause of the housing crisis is the result of increasing demand (humans population) for a finite resource (land). Using more of the finite resource, without reducing demand for that resource, increases the scarcity of the finite resource. The only way to actually address the cause of the crisis is to reduce demand for the finite resource.